Home

Categories

A - Luxury Watches

B - Digital Banking

C - Best Web Hosting

D - AI Tools / No-Code Tools

Z - Blog

Reviews

Promo Code

Best Products 2026

Deals & Offers

Updates

Admin Login

User Login

Home

Trusted Reviews & Smart Shopping Guide

Find the Best Top Brands Online | Mujaiyana Media

How to Choose the Best Domain Name and Web Hosting...

Creating a professional website begins with two essential decisions: choosing the right domain name...

The Future of Luxury Fashion in 2026 How Premium S...

In 2026, luxury fashion is no longer just about expensive clothing or famous designer labels. It has...

The Future of Digital Opportunities AI, Online Bus...

The world is entering a new digital era where technology is changing the way people live, work, and...

Digital Business Growth in 2026 Essential Tools fo...

The digital world is creating new opportunities every day. Today, entrepreneurs, startups, freelanc...

Tesei Titanium Automatic – A Modern Dive Watch Bui...

Luxury dive watches continue to attract collectors, professionals, and watch enthusiasts around the...

Fleuss Dive Watch – Vintage Inspired Automatic Wat...

The Fleuss Dive Watch is a timepiece that blends the charm of the golden age of diving watches with...

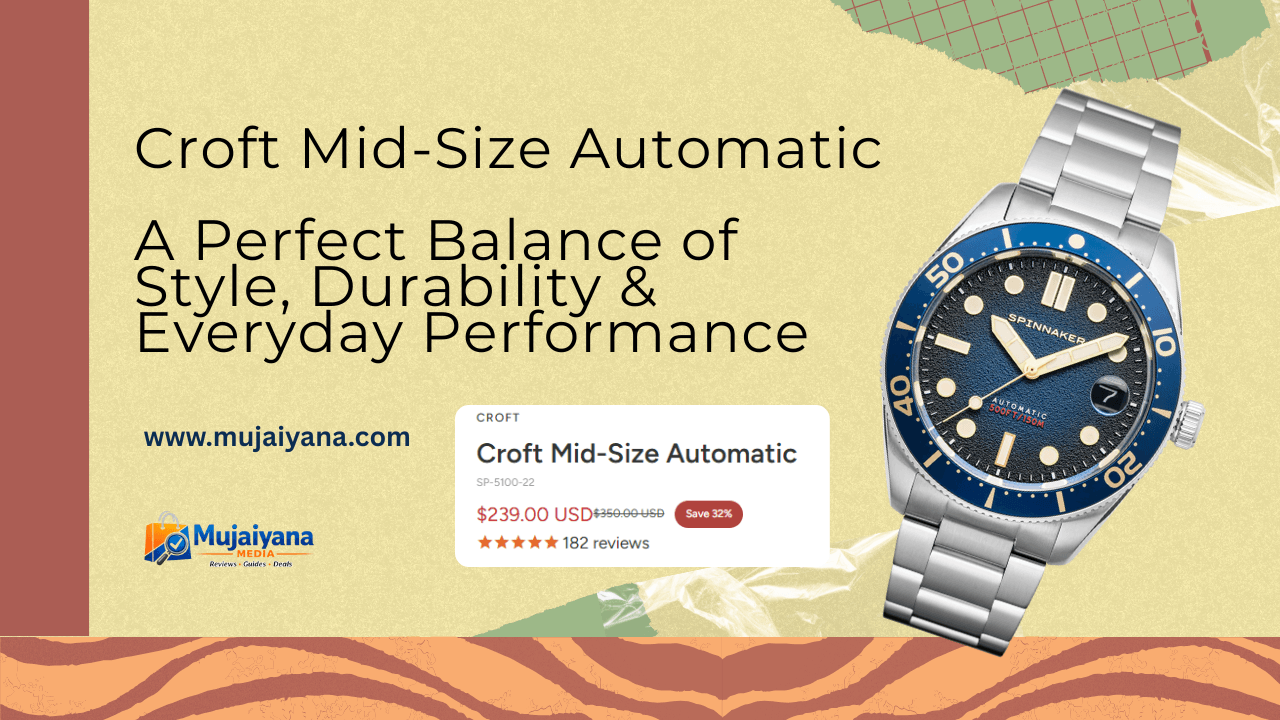

Croft Mid-Size Automatic – A Perfect Balance of St...

When it comes to automatic watches that combine classic diving heritage with modern everyday usabili...

Modern Domain & Hosting Platform for Startups – Wh...

Mujaiyana.com is a growing digital platform under Mujaiyana Media, focused on smart online tools, we...

Best Web Hosting for Beginners in 2026 – Why Hosti...

Mujaiyana.com is a modern digital platform under Mujaiyana Media, focused on smart online tools, AI...

The Future of No-Code Website Building in 2026 – H...

Mujaiyana.com is a modern digital knowledge platform under Mujaiyana Media, focused on smart online...

AI Website Builder Revolution in 2026 – How No-Cod...

Mujaiyana.com is a modern digital platform under Mujaiyana Media, where we explore smart online tool...

How AI Website Builders Are Changing Online Busine...

Mujaiyana.com is the official platform of Mujaiyana Media, where we explore smart digital tools, mod...

Simple Global Digital Banking Platform for Freelan...

Managing money internationally is no longer a luxury—it is a necessity for freelancers, remote worke...

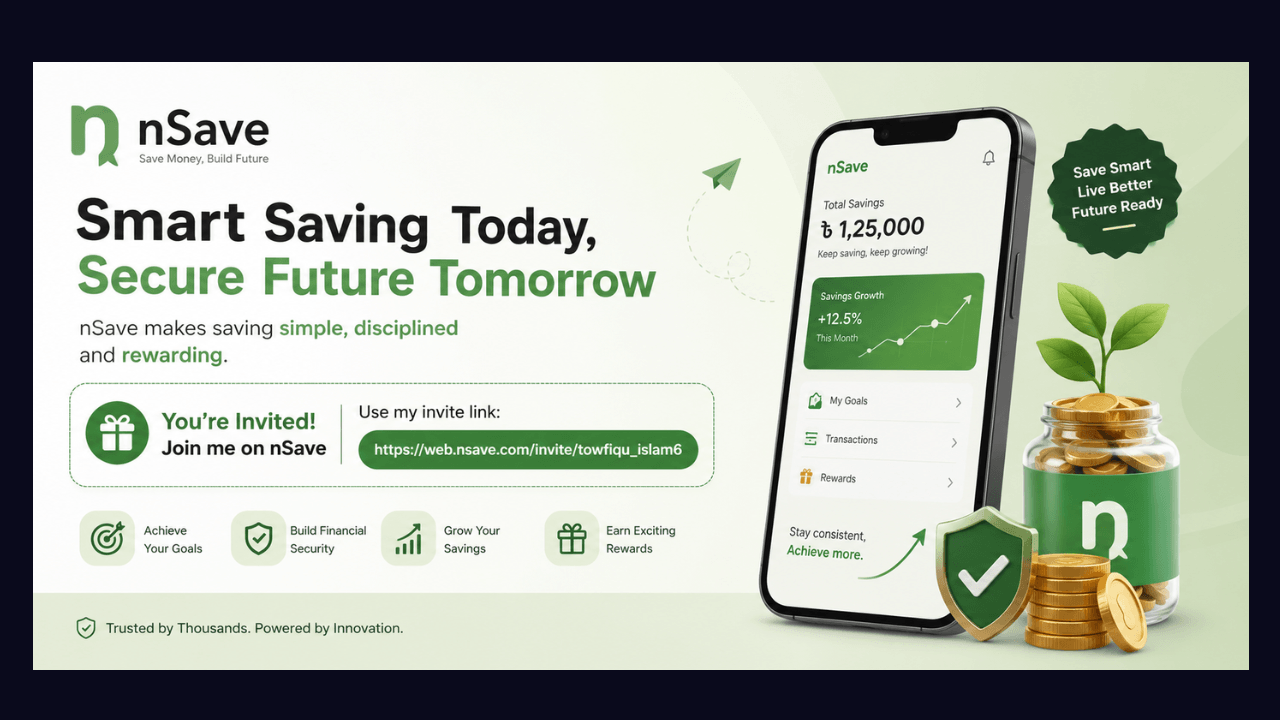

nsave Review 2026: A Modern Way to Manage Global M...

In today’s digital world, managing money across countries has become a real need for freelancers, re...

Why nsave Is Getting Popular Among Global Users in...

Managing international money transfers, global payments, and multi-currency accounts has become incr...

Why Spaceship Is Becoming a Popular Choice for Dom...

Why Spaceship Is Becoming a Popular Choice for Domains & Hosting in 2026Launching a website star...

Hull Chronograph (Pine Green) Review – Stylish Lux...

Hull Chronograph (Pine Green) – A Bold Timepiece for Modern Watch LoversIf you are looking for a sty...

Spinnaker Hull Chronograph Review: Bold Design Mee...

If you are a watch lover or someone looking for a stylish timepiece without spending a fortune, Spin...

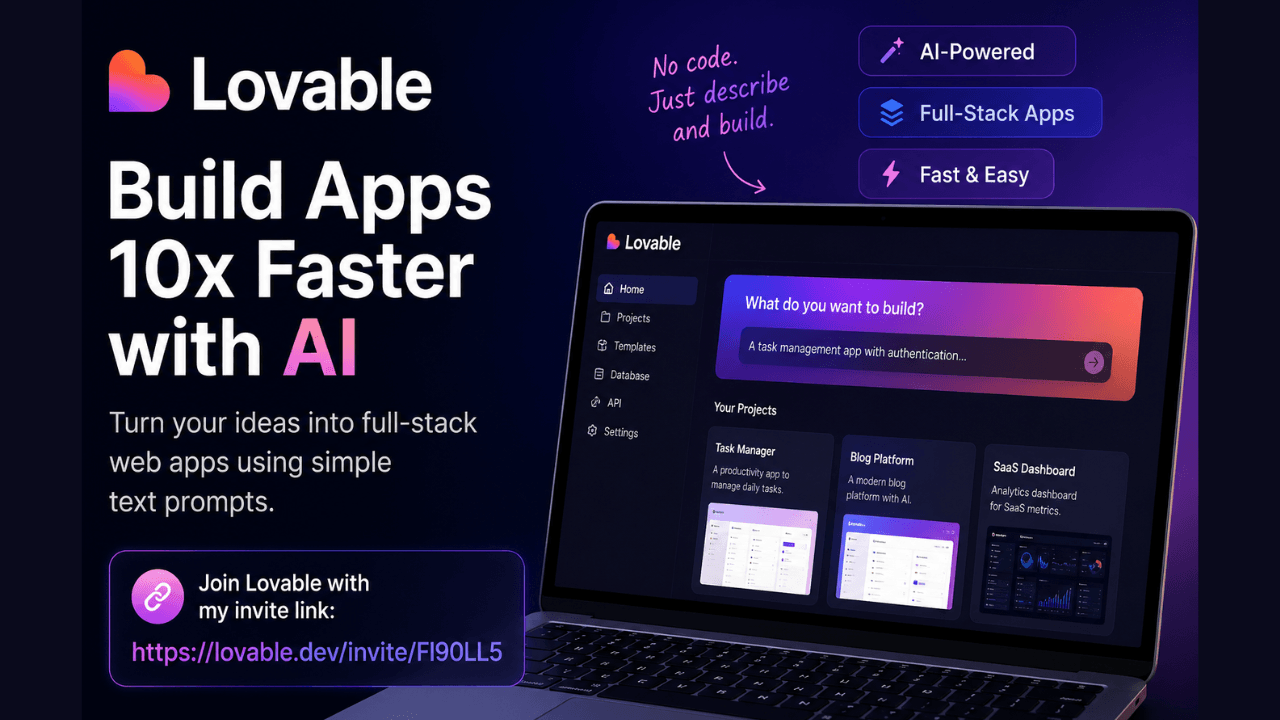

Smart AI App Building with Lovable: A Simple Way t...

In today’s fast-moving digital world, building websites and applications has become much easier than...

New Era of Banking: Why You Should Try NSave Today

In today’s fast-moving digital world, traditional banking is slowly being replaced by smarter, faste...

‹

1

2

3

4

5

6

7

8

›